COVID-19 in context: Only the strong survive?

Last month, Moody’s released an investor update headlined, “Universities with strongest brands, significant scale, highest debt levels best positioned for coronavirus challenges.” While that may be true for the strongest universities, the increased demand for higher education that will inevitably follow the COVID-19 pandemic means that institutional relevance and the agility necessary to respond to shifting market dynamics will be just as important as scale of brand and strength of the balance sheet when it comes to survival.

As a consequence of COVID-19, demand for higher education will increase—not diminish. However, one of the legacies the pandemic will likely leave behind is a generation of students much more focused on the returns their education will deliver—especially when it comes to serving the needs of a global student body.

In a thought-provoking article in New York magazine, Scott Galloway, Professor of Marketing at New York University’s Stern School of Business, projects that coronavirus will bring on a period of accelerated disruption in which institutions that he refers to as Tier 2 colleges will disappear, succumbing to the same fate as retail malls in the United States in the face of competition from online disruptors like Amazon. Meanwhile, he argues, mega-education brands will collaborate with big tech to drive more change and pressure on pricing models. It’s a compelling story, but I’m not totally convinced.

There is no doubt that universities and colleges across the globe are facing a significant challenge as a result of COVID-19, as this piece in the Australian Financial Review, or this in the UK’s Financial Times illustrate.

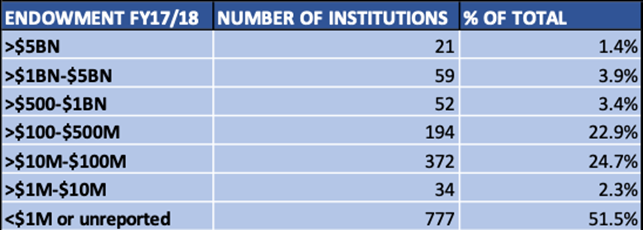

In the U.S., it will be especially difficult for universities with small endowments that depend on the full tuition most international students pay to deal with the temporary enrollment decline and increased competition that will follow COVID-19. Contrary to what most external observers believe, the overwhelming majority of U.S. universities do not have a meaningful endowment upon which to rely. More than half have an endowment of $1 million or less, and less than 10% have endowments exceeding $500 million.

Source: IPEDS

In addition, like public universities like these in Arizona, Pennsylvania, Louisiana and Oklahoma face multiple rounds of cuts in state appropriations. Those that have historically turned to international students to subsidize financial aid for domestic students and weather reduced funding may find the short term particularly difficult to navigate.

They aren’t alone. Regardless of jurisdiction, universities in Australia, the U.K., Canada, and popular study destinations all rely on the revenues that international students bring to their campuses and wider communities to some extent. Lest we forget, the presence of international students contributes much more than tuition revenue. David di Maria, Associate Vice Provost for International Education at the University of Maryland, Baltimore County sets out very clearly the value of international students and the risks of losing them in The Conversation.

Demand has not disappeared

One defining aspect of the COVID-19 crisis has been an understandable desire to focus on the immediate. My personal universe has shifted from commuting across the Atlantic twice a month to never wandering further than two kilometers from my home. Likewise, there has been a complete focus on the immediate gloom surrounding this fall’s enrollment and the associated handwringing on the future of global higher education. It can be tempting to believe this disruptive moment will never pass and that the world and demand for education has shifted permanently. This analysis, from the UK’s Higher Education Policy Institute, (HEPI) published on 9th June indicated that 85% of students are “itching to get back on campus” and, when taken with the myriad of other surveys suggests a pent-up demand waiting patiently for the green light to resume their studies. As originally planned.

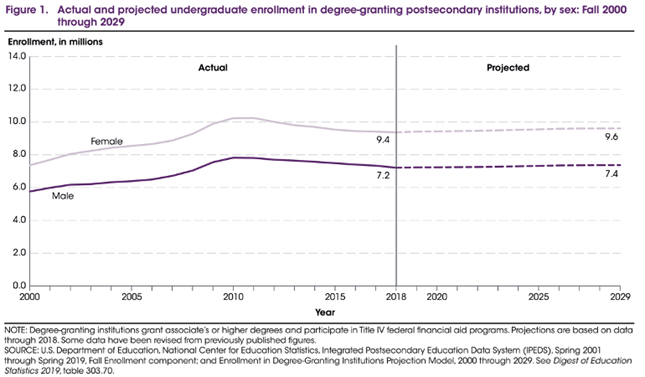

It is also useful to remind ourselves that the scale of higher education participation and long-term need still remains. A report released on May 26th by the National Center for Education Statistics forecasts that total undergraduate enrollment in the U.S. will increase to 17 million students by 2030. Granted, this is a much lower rate of increase than the preceding decade, but it still means a lot of students to serve. And, it is difficult to imagine they will all go online or fundamentally question the value of higher education. In fact, as State Higher Education Executive Officer Association (SHEEO) data shows, demand for higher education tends to be counter-cyclical, with participation increasing as economies weaken.

Source: National Center for Education Statistics

Jo Johnson, the former UK Universities minister and current fellow at Harvard and King’s College London reminds us in a recent blog of the sheer scale of global demand. It is worth re-sharing his analysis:

“Driven by growth in middle classes in developing countries in Asia and Africa, the demand for higher education is set to increase from 160 million students in 2015 to over 414 million by 2030, according to UNESCO. To meet that surge, the world would have to build four universities that serve 80,000 students every week, every year.

The two largest nations in the world, China and India, which account for a quarter of overseas students, cannot accommodate student demand for higher education within their borders. (This year’s Gao Kao, China’s national university entrance exam, if it takes place, will have more than 10 million students competing for no more than eight million places.) They are far from unique.

In Bangladesh, a country with a young population of 170 million, and Sri Lanka, there are an estimated five students competing for every available university place, according to the British Council.”

Meeting that demand will require more than a strong brand and deep pockets. Understanding what drives mobility, responding to changing student demand, and having ability to reach those students—either through an institution’s own resources or in partnership with those that can provide that reach and global expertise – will be critical.

A need to understand the key drivers, and access to market

The core drivers of global demand for higher education remain unchanged. At a macro level, students are largely driven by a fundamental belief and ambition that education—especially high-quality education—improves life prospects. Mobility, in turn, is driven by affordability and access.

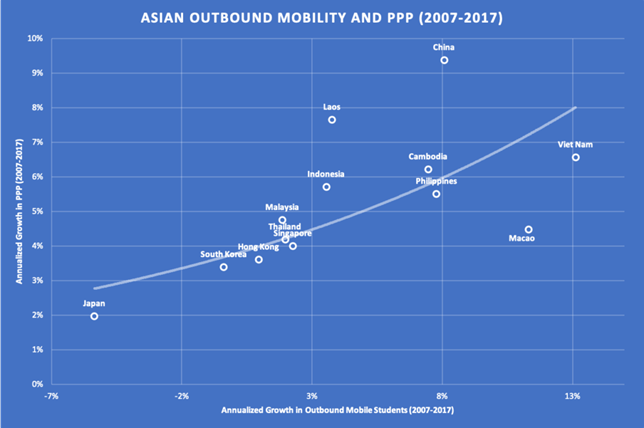

As the chart on East Asian countries below illustrates, there is a clear and unsurprising correlation between a growth in Purchasing Power Parity and Outbound Mobility. As personal wealth increases, so too does outbound student mobility—especially where there is a lack of local capacity. China and Vietnam are perfect examples of that phenomenon in action.

Source: UNESCO UIS.Stat

Increasingly, it is the rapidly developing economies of South and Central Asia and sub-Saharan Africa where demand will increase and which local capacity is still unable to serve.

However, there is much more to this equation than affordability and capacity. In a universe of choices, understanding what really motivates students is critical—especially when affordability is compromised by global recession, or depression, if some of the bleaker forecasts of the COVID-19 impact are to be believed.

Aspiration and employability drive mobility

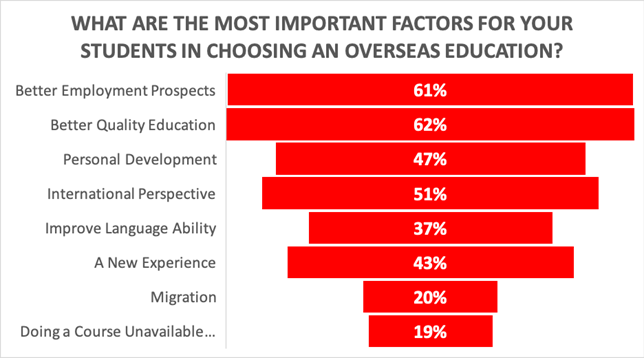

In a blog post last year, we dissected a global agent survey based on almost 2,000 responses to identify what drives students from multiple countries to study overseas. For most, it is the pursuit of a better-quality education, an international perspective, and enhanced employment prospects. We put out another survey in February 2020, and the results are laid out in the charts below.

Source: INTO Global Agent Survey, February 2020

Mobile students are looking for education which improves their career outcomes. We should be careful not confuse employability with migration. That is clearly a driver for some parts of the world. But the desire to gain some work experience overseas as part of a wider education experience is as much about burnishing one’s resume for long term employment in their home country as it is about planning to settle elsewhere.

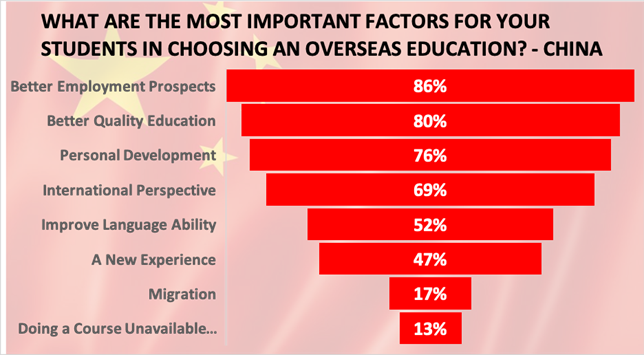

Take China, the world’s largest source market. Recent research published by Bonard indicates that more than 85% (3.64 million) of Chinese students educated overseas return home to pursue their careers. This corresponds with our own research in which less than 17% of (425) China-based agents identify migration as a factor for their students.

Source: INTO Global Agent Survey: February 2020.

It is not a given that these needs will be addressed by the strongest brands necessarily. As Charles Darwin famously observed, it’s not always the strongest of the species who survive, nor the most intelligent, it’s those most adaptable to change. We saw evidence of that in South East Asia in the aftermath of the Asian Currency Crisis and this time, innovations in online delivery, flexibility in academic calendars, new institutional partnerships will unlock opportunity for institutions and students alike. Those with agile business models, an unswerving focus on delivering great experiences and with more than eye on the ultimate outcome students seek are likely to thrive in the coming years.

R.E.A.P. the benefits.

When asked, at a recent seminar hosted by University of California at Berkeley what we believed were the characteristics for success, we identified four.

1. Resilience

This fall will be a challenge for students and institutions like never before. We need to remember that even though students may defer or have some second thoughts about when the best time is to study, they still intend to continue. Most surveys, including this from QS indicate that desire to go overseas increases rather than diminishes as the lockdowns and travel restrictions persist. Institutional resilience, in terms of retaining their international student infrastructure to address student questions, manage to delayed enrollment funnel and engagement.

2. Empathy

There is barely a human on the planet unaffected by the pandemic. Understanding that for international students, they face a set of additional challenges – travel restrictions, securing visas, receiving acculturaltion support as well as online instruction is central to any response. Most important, Gen Z students, who’s education has been profoundly disrupted by COVID, will have the same service expectations they were accustomed to before the pandemic took hold. And, based on the evidence we have seen, it is unlikely that a purely online alternative, no matter how well-designed or delivered will be enough.

3. Agility

If this crisis has taught us anything it is, that as a society and as a sector, when the chips are down and the challenges greatest, we have risen to them. Change in higher education can sometimes take years to affect and a recognition of change and preparedness to pivot pre-existing strategy will be crucial . Alex Usher, the Canadian strategist reminded us in his blog the other day, of Mike Tyson’s perspective on strategy, “Everyone has a plan until they get punched in the mouth.”

Now, most higher education has transitioned to online learning and support. Some, such as the University of Arizona in the United States have gone further, accelerating their Global Campus developments , a seriously ambitious project to meet student demand online, on -campus or in a hybrid blending Arizona content with local support and the student experience offered by their partner universities across the globe. In the coming year, those schools which can show flexibility on start dates, have thought through issues such as quarantine for international students when they arrive on campus and have put in place thoughtful contingencies which reflect those students’ unique challenges are much more likely to retain more of their international incoming class.

4. Partnership

Like most things in life, challenges can appear less daunting and opportunity greater when faced together. As institutional budgets are challenged and immediate focus lies elsewhere, universities committed to meeting the global education need and committed to innovative approaches will find organizations who share common cause and can also provide access to the resources, reach, technologies and expertise which enables them to provide higher education opportunity to the millions of students in the aftermath of this crisis.